Pension fund socialism for AGI

AGI economy series - Nr. 10

Would you believe me if I told you that the United States secretly has a socialist economy?

Well, don’t take my word for it; take it from Peter Drucker, father of modern management theory. In his 1976 book The Unseen Revolution: How Pension Fund Socialism Came to America Drucker observed that through the expansion of employer-sponsored pensions, pension funds had become some of the largest holders of corporate stocks. This shift meant that millions of workers, through their retirement savings, indirectly owned a significant share of the American economy.

Drucker described this as a form of "pension fund socialism" because the workers, through these funds, effectively collectively owned a part of the means of production, even though they were managed by financial institutions. Unlike the government-led socialism of the Soviet Union or other command economies, pension fund socialism was driven by market forces.

This democratization of capital ownership allows a large portion of the population to benefit from stock market returns. In a future scenario, where AGI might cause a decline in the labor share of income, the broad participation in pension fund investments could ensure that more individuals benefit from investment returns. This in turn reduces the pressure on public social security benefits.

The three pillars of pension systems

Every national pension system is different. However, in general pension systems consist of a mix of three pillars:

First pillar: Avoiding poverty in old age (mandatory, state-sponsored). In most countries the first pillar is a public pension system where current workers' taxes fund retirees' benefits (pay-as-you-go). In the US context this would be Social Security (formally the federal Old-Age, Survivors, and Disability Insurance), where benefits depend on a worker’s years of contributions and earnings history over their lifetime, but are designed to provide a basic income floor rather than a direct replacement of pre-retirement earnings.

Second pillar: Occupational pensions (encouraged or mandatory, employer-sponsored). The second pillar should provide an adequate replacement of labor income for people with normal labor market careers. Employers often offer retirement plans like 401(k) or traditional defined benefit pension plans. In 401(k) plans, employees contribute a portion of their salary, often with employer matches. The plans are mostly invested into stocks & bonds. Pay-as-you-go occupational pensions are not widespread, however, there are specific contexts such as certain public sector schemes, where occupational pensions are also financed by current workers' contributions rather than being pre-funded.

Third pillar (voluntary, individual savings). The third pillar leaves room for individual savings to top up the retirement income. Individuals can often contribute to tax-advantaged accounts like IRAs (Individual Retirement Accounts), which offer additional private saving opportunities outside employer plans, mostly invested into stocks & bonds.

Countries should reduce their dependence on pay-as-you-go

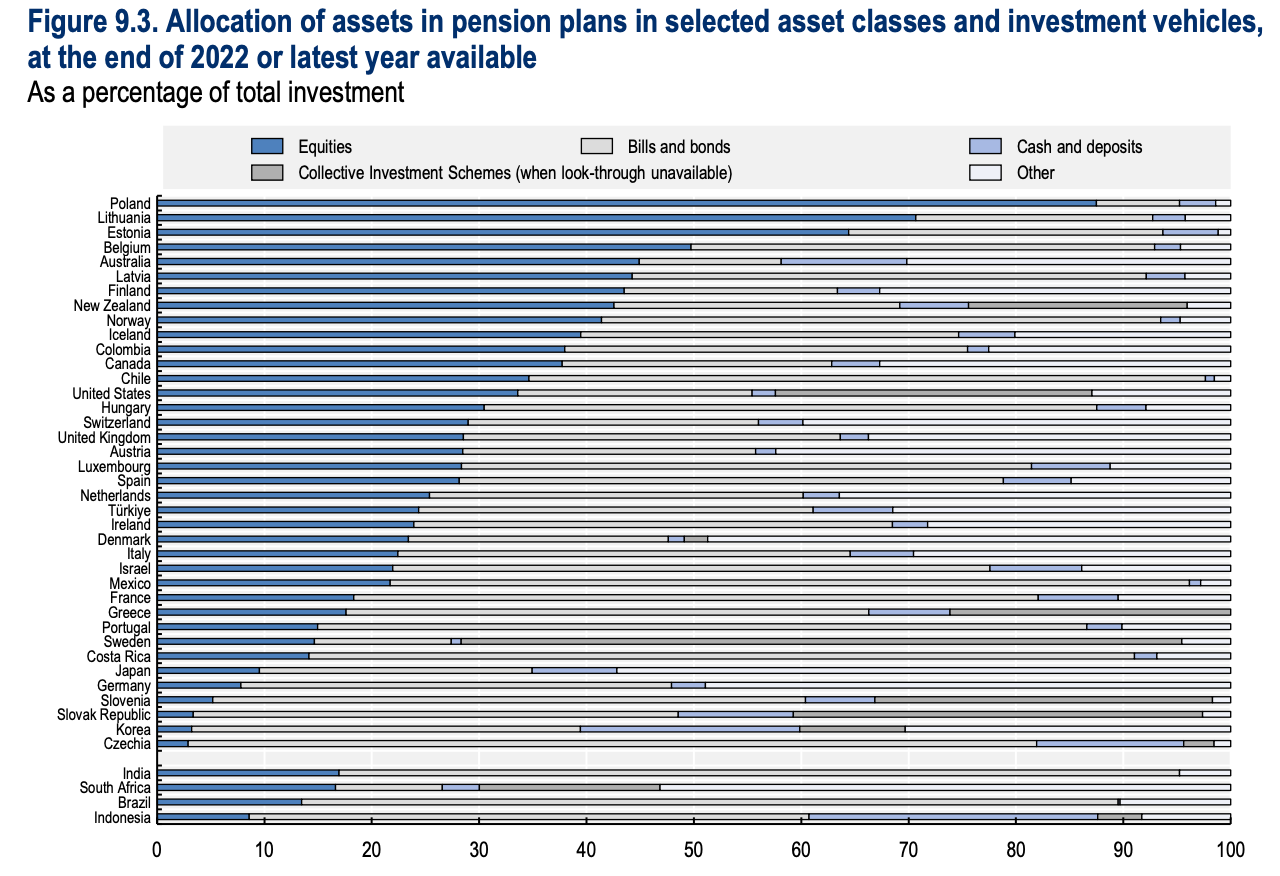

Some pension systems, such as those in Singapore or Chile, have a very high exposure to stock markets and other financial assets. This means individuals are forced or incentivized to invest a significant share of their current labor income in the stock market to live off capital income in a post-work phase of their lives. In contrast, the pension systems in countries like France or Italy heavily rely on a pay-as-you-go system for their pensions. In pay-as-you-go systems pensions are intergenerational transfers, where young generations transfer a part of their labor income to older generations.

Pension systems treat the labor income that backs pay-as-you-go systems as an infinite economic resource. However, this is neither true based on demographics, nor workable in the event of a highly automated future economy. In an AGI scenario, the share of labor income might be significantly reduced, and the share of capital income might be significantly increased. The cautious, long-term perspective is to treat labor as a finite source and that means we want to follow Hartwick’s rule and transform it into an infinite source by investing it in markets. Hence, countries should consider reducing the dependence of pension systems on pay-as-you-go funding and increasing the exposure to stock markets. There are multiple ways to achieve this:

a) Reducing the weight of the first pillar

The classic way to reduce reliance on pay-as-you-go is by increasing the weight of the second pillar (occupational pensions). The most famous example of a structural pension reform from a pay-as-you-go system to more market exposure is Chile’s 1980 pension reform. Countries don’t necessarily need to make such a radical shift, but pension reforms take time and at a minimum countries should not rely on pay-as-you-go for the majority of pension payments. This is especially relevant for some European countries with very high reliance on the first pillar, such as France, Italy, and Spain. Getting from somewhere between 70-90% pay-as-you-go dependence closer to 30-50% like Switzerland, the Netherlands, or the UK, would be a meaningful shift.

b) Decoupling the first pillar from pay-as-you-go

Having an insurance against poverty in old age is still relevant. So, we should not abolish the solidarity goal of the first pillar, even if the prevalent way to finance the first pillar via a pay-as-you-go system does not seem sustainable in the long run. Rather the social goal and the financing mechanism are two issues that can be separated. For example, countries could implement a mandatory Pillar 1 system where worker contributions are pooled and invested in a public fund, whose returns fund Pillar 1 solidarity. For example, the Central Provident Fund of Singapore combines Pillars 1 & 2 in a unique way, providing basic social protection while also being a mandatory savings scheme linked to earnings.

c) Increasing stock market exposure of the second pillar

There are significant cross-country differences between how risk averse pension funds are. The optimal risk averseness should also depend on age (see e.g. “100-120 minus your age rule”). Still, it seems that pension funds in many countries are cautious and could reasonably increase average stock exposure to something closer to 50%.

Overall, a move towards more “pension fund socialism” through strengthening pillars 2 & 3 and reforming the financing of pillar 1 has two big advantages in the context of AGI. First, it gives more people exposure to the financial upside through the stock market. Second, pension systems with a lower share of pay-as-you-go systems are much better prepared for an economic shock that could lead to a significant decline in the labor share of income.

Thanks to

& for valuable feedback on a draft of this essay. All opinions and mistakes are mine.

Nice read Kevin. This is a sound proposal and I may incorporate some of these ideas into my own essay on the topic: https://www.lianeon.org/p/rethinking-social-security

I suggested a two-tier system where there is a low, albeit transparent, payout to individuals when they retire. The majority of their income, however, would be their responsibility to save. The government would aid this by offering a “portable 401k” account that followed the employee, not the employer.

Tax advantaged, low or zero fees, and automatic enrollment would preserve the incentive to work and save, a small “nudge” that would greatly reduce the reliance on the first tier.

An expanded version of this could be helpful in an AGI scenario.